In 2016, there was a clear upward trend in the fight against tax evasion globally. The April 2016 release of the Panama Papers caused an international shake-up that resulted in multiple global tax evasion investigations and regulatory reviews including in the British Virgin Islands, Singapore, Hong Kong, France, Spain, Germany, Australia, Austria, Sweden and the Netherlands.

The US also continued to focus its efforts on offshore tax evasion and has made significant progress in combating it through its Swiss Bank initiative, various OVDP programs and FATCA.

In addition to investigations and prosecutions, governments are continuing to employ tools such as amnesty programs and global tax reporting mechanisms to learn new information about undisclosed account holders and the institutions and structures that either knowingly or passively aid them.

As a result, governments now have unprecedented access and insight into the historically hidden world relating to the maintenance of offshore accounts. This includes the identification of previously unreported individuals and corporations, and information about the financial institutions (“FIs”) and advisors that they use.

Governments are also beginning to share information amongst each other about tax evasion activities outside of traditional regulatory platforms. The Joint International Taskforce on Shared Intelligence and Collaboration (JITSIC), met in Paris to conduct the “largest ever simultaneous exchange of tax information and to share results and details on thousands of investigations sparked by the Panama Papers.” The meeting is reported to have resulted in the creation of a “target list” of 100 lawyers, bankers, accountants, and other advisors who enable the use of tax havens.

The JITSIC brings together 37 of the world's national tax administrations that have committed to more effective and efficient ways to deal with tax avoidance. It offers a platform to enable its members to actively collaborate within the legal framework of effective bilateral and multilateral conventions and tax information exchange agreements, sharing their experience, resources and expertise to tackle the issues they face in common.

The JITSIC brings together 37 of the world's national tax administrations that have committed to more effective and efficient ways to deal with tax avoidance. It offers a platform to enable its members to actively collaborate within the legal framework of effective bilateral and multilateral conventions and tax information exchange agreements, sharing their experience, resources and expertise to tackle the issues they face in common.

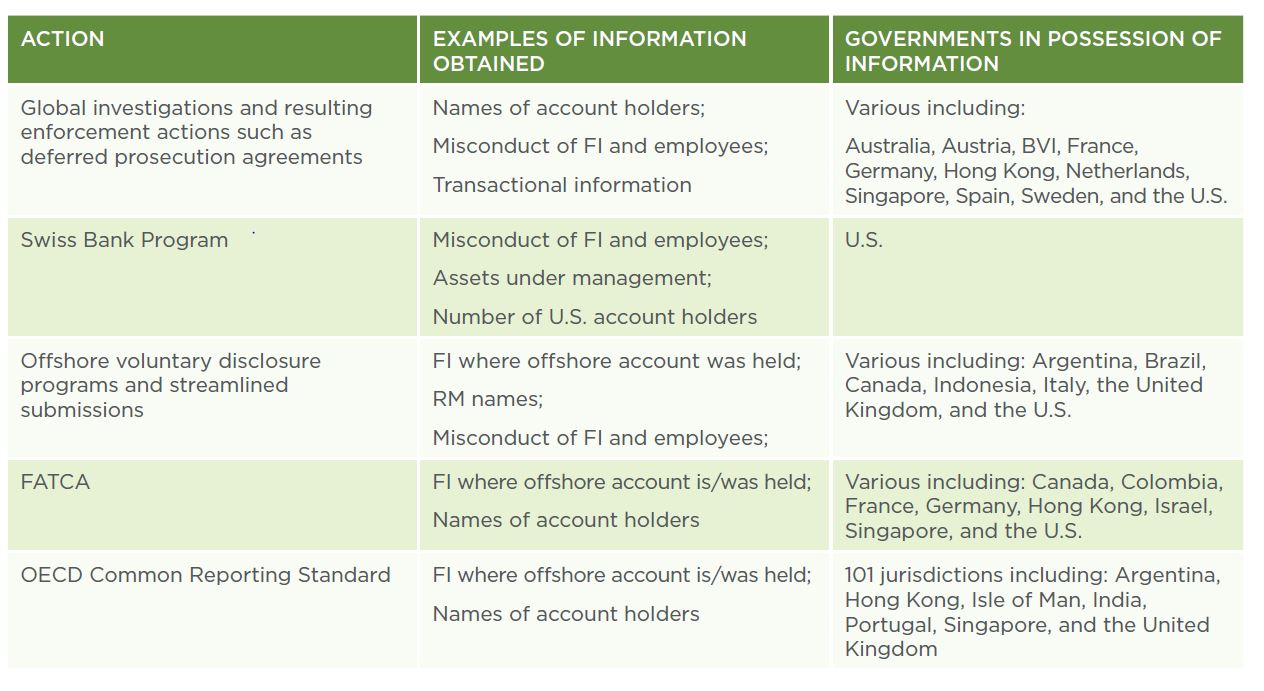

With this new access and insight into the once hidden world of undisclosed offshore accounts is at unprecedented levels.

In the course of these Investigations of

Individuals and Financial Institutions (FI),

Individuals and Financial Institutions (FI),

Governments are learning "Valuable Information" about Previously Undisclosed Offshore Account Holders and

the Institutions that HELPED them.

This information is summarized in the following chart.

We previously posted 145 Offshore Banks & Now Financial Advisors Are Turning Over Your Names To The IRS - What Are Your Waiting For? where we discussed that the IRS keeps updating its list of foreign banks which are turning over the names of their US Account Holders, who are now subject to a 50% (rather than 27.5%) penalty in the IRS’s Offshore Voluntary Disclosure Program (OVDP).

Within the OVDP, people who

Pre-Cleared

Before the various Effective Dates

are generally Safe From the

Higher 50% Penalty.

Higher 50% Penalty.

As additional banks are added to the list, only those American taxpayers that request pre-clearance before their bank is listed, will get the 27 1/2% OVDP penalty. The 50% penalty now applies to all taxpayers with accounts at financial institutions or with facilitators which are named, are cooperating or are identified in a court filing such as a John Doe summons.

Although the 50% penalty is high, willful civil violations can result in tax, penalties and interest totaling 325% of the highest balance in the account for the most recent six years period. Recent guidance suggests that the IRS could be more lenient in the future, but the IRS’s definition of leniency can still make the OVDP a very good deal that provides certainty.

Do You Still Have Undeclared Income from

Offshore Banks or Financial Advisors?

Want to Know if the OVDP Program is Right for You?

Contact the Tax Lawyers at

Marini& Associates, P.A.

for a FREE Tax Consultation

at: www.TaxAid.com or www.OVDPLaw.com or

Toll Free at 888-8TaxAid (888) 882-9243

ACTION

Read more at: Tax Times blog

{kind=link}

{kind=link}