The fourth quarter 2018 citizenship renunciation numbers have been published by the Office of the Federal Register. What these numbers mean and how they differ from recent trends.

The fourth quarter 2018 citizenship renunciation numbers have been published by the Office of the Federal Register. What these numbers mean and how they differ from recent trends.

Why Do Expats Care About Citizenship Renunciation?

Every quarter, the Federal Register publishes an update of American citizens who have renounced their citizenship. Citizenship renunciation is an issue that especially affects expat since they are faced with the lifelong burden of reporting American expatriate taxes (and sometimes, depending on the amount of income the expat generates, a tax paying burden as well!). Currently, the only way to rid themselves of this requirement is to renounce citizenship – a very permanent decision.

For a long time, expats have wanted to have a bigger say in the political sphere about tax fairness, but have felt ignored by politicians and are stuck with a requirement to pay or report American expatriate taxes.

The stakes are particularly high for expats, who are often unaware of the lingering filing requirements and can have their passports revoked if they are too far behind on filing American expatriate taxes.

Recently, the Tax Fairness for Americans Abroad Act was proposed, which would exempt expats’ foreign earned income from US taxation. Though this is good news, the bill is still far from becoming law, and for now, renunciation is the only recourse to what many feel are unfair taxation and financial reporting requirements.

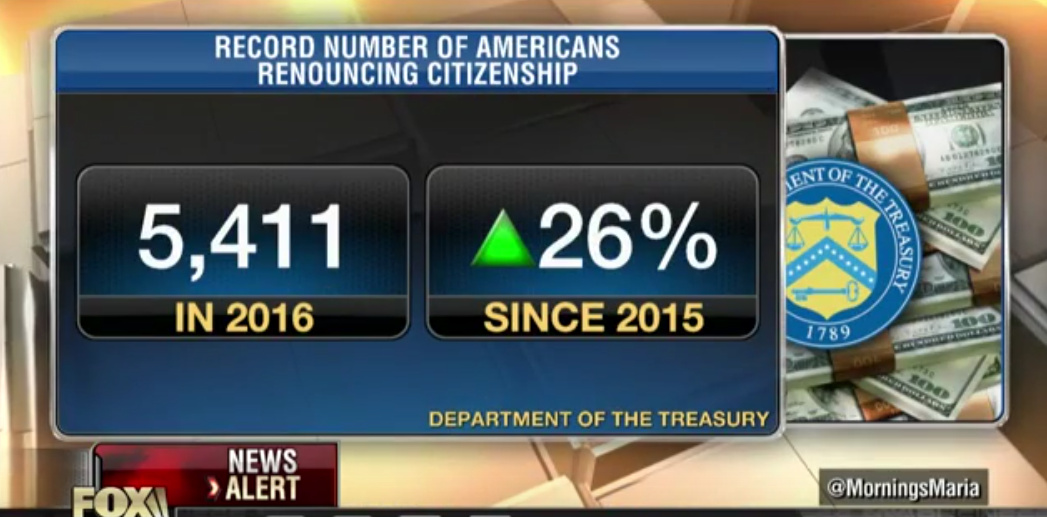

A Brief History of Citizenship Renunciation Numbers

In 2017, the breakdown of the 5,132 renunciation numbers was as follows:

- Q1: 1,313

- Q2: 1,758

- Q3: 1,376

- Q4: 685

In 2018, the 4,050 renunciation numbers were:

- Q1: 1,168

- Q2: 1,093

- Q3: 1,104

- Q4: 685

Overall, in 2018 the numbers were lower than 2017 by around 20 percent, so it seems that, in general, we’re experiencing a return to more normal renunciation rates.

However, the fourth quarter drop off occurred again, suggesting that expats and American residents in general don’t renounce as often in the fourth quarter, whatever their reasons may be.

Perhaps the last three months of the year are so holiday-laden that Americans worldwide find their wallets light and the expense to renounce too much to bear. The cost to renounce is $2,350 after having undergone a 422% increase in 2015, which is the highest fee in the world. Plus, if you meet certain thresholds, you may also have to pay the exit tax, which can be extremely costly. The thresholds are met if any of the following are true:

- Your average annual net income tax for the five years before the date you renounce exceeds a certain amount that is adjusted for inflation each year (in 2018, the amount is $165,000).

- Your net worth is $2 million or more on the date of your expatriation.

- You did not certify on Form 8854 that you are fully compliant with your US tax obligations for the five years prior to your expatriation.

The way the exit tax is calculated is by deeming all your assets sold on the day before you expatriate; you would then be taxed on the associated capital gain, which can be taxed at a rate as high as 23.8%. But for some, this is still the best option in order to bypass the reporting and financial headaches that come along with American expatriate taxes.

Marini & Associates, P.A.

Read more at: Tax Times blog