According to Law360, high-net-worth individuals may find themselves the focus of unwanted attention from the Internal Revenue Service. Last summer Douglas O'Donnell, the commissioner of the IRS Large Business and International, or LB&I, Division, announced the IRS would begin a new campaign initiating several hundred audits of high-net-worth individuals.

The new examinations will be conducted by a specialized group of examiners in the global high wealth industry group at LB&I nicknamed "the Wealth Squad." The Wealth Squad specializes in taking a holistic approach and examining the types of complex financial transactions and holdings that are more common among high-net-worth individuals.

As the Wealth Squad sends out notices to targeted high-net-worth individuals, professional advisers need to be prepared to develop an effective strategy for representing these clients through the audit process and beyond. That strategy includes making a high-level review of their clients' business and financial holdings, identifying potential issues, developing the roles that respective professional advisers will play during the audit, and how to best respond to requests for documents or interviews with their clients.

One of the most important items during the examination is to ensure that the taxpayer is protecting any privileged communications and preserving objections to the government's requests in the event of any future litigation.

LB&I has an established examination process that outlines the phases of an LB&I examination and the steps that occur during each stage. Professional advisers should review the LB&I examination process to help them formulate their plan for representing their clients through the examination.

Among those campaigns are issues related to offshore holdings and foreign transactions; syndicated conservation easement transactions; Internal Revenue Code Section 831(b) captive insurance companies; private foundation abuses; and S corporation issues related to excess losses, built-in gains and shareholder distributions.

By identifying these issues early, professional advisers are able to identify other parties that may have information relevant to that issue and work to gather any relevant documents, ensuring they have adequate time to review the information and develop a strategy addressing the potential issue.

Upon identification of issues that may become a focus of the audit, a decision needs to be made as to who among the taxpayer's professional advisers is in the best position to handle the examination and interact directly with the IRS. Section 7521(c) grants the representative the right to handle any interview without the taxpayer present, absent a summons, and the professional adviser should limit direct interaction between their client and the examiner.

In large cases that are likely to end up in litigation, an attorney should be engaged early to help develop a strategy for the audit with an eye towards litigation. If there is any hint that anything in the audit could be construed as some form of fraud or misrepresentation by the taxpayer, everything must stop immediately, and the attorney who handles criminal tax defense needs will advise on how to proceed.

One of the most important aspects of an examination is to maintain privileges and preserve objections in the event of any future litigation. Section 7525(a)(1) extends limited protection to certain tax-practitioner communications for noncriminal tax matters if such communication would have been privileged if it were a communication between a taxpayer and an attorney.

When An Attorney Has Been Engaged, The Parties Should Execute A Kovel Agreement To Extend The Attorney-Client Privilege To The Taxpayer's Nonattorney Professional Advisers.

Given the likely complexity of a high-net-worth taxpayer's business and financial holdings, there are likely to be a number of potential professional advisers to assist in the audit, each of whom should enter into a Kovel agreement to protect their audit-related communications.

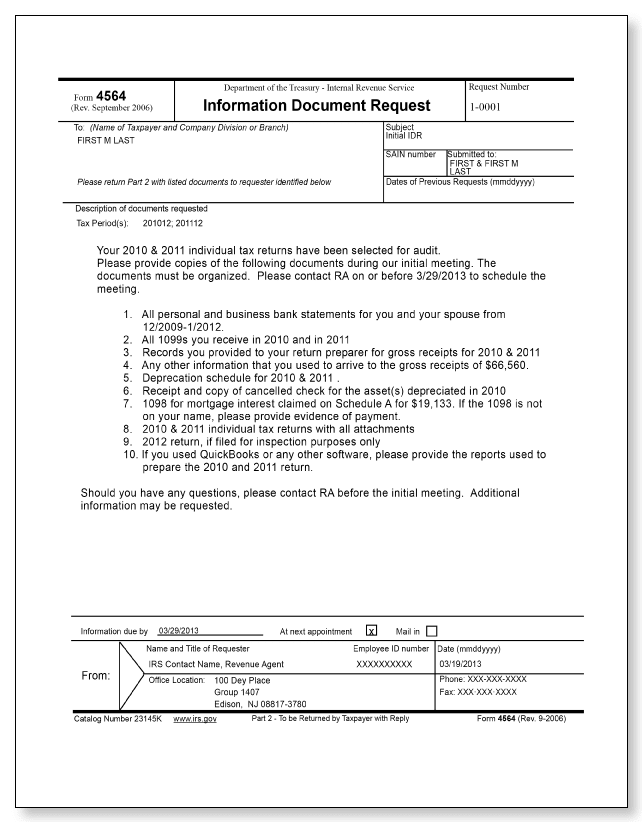

Following the initial audit notification from the Wealth Squad, the examining agent is likely to begin making requests for documents related to the taxpayer and their business and financial holdings. Unlike a summons, an information document request has no statutory authorization outside of the general power of the IRS to examine returns.

However, timely responses to information document requests help establish cooperation and reduce the likelihood that the government will feel the need to issue a summons. It is important during this stage to maintain objections to any requests and preserve privileges.

Among the potential objections are that the requests are overly broad, unduly burdensome or vague, that the request has provided inadequate time to comply, or that the documents are not within the taxpayer's possession, custody or control.

If the requests come in the form of a summons, the government must be able to establish that it was issued for a proper purpose, that the information sought is relevant to an existing examination, that all administrative and statutory procedures have been satisfied, and that the information is not already in the possession of the IRS.

The IRS cannot compel taxpayers to waive privileges, however, any conduct by the taxpayer or their representative that is inconsistent with the maintenance of privilege can operate as a waiver.

The overarching goal while representing a high-net-worth individual in an audit is to cooperate with the examiner and the government's requests for documents while protecting your client by preserving objections and privileges. Cooperation does not mean waiving privileges, statutory limitations periods or other rights that protect taxpayers.

High-net-worth individuals receiving audit notifications from the Wealth Squad should be prepared for a thorough examination of their business and financial holdings that includes their personal information along with information from any entities in which they hold an interest, including any domestic or foreign corporations, partnerships, trusts or charitable foundations.

Using the resources published by LB&I, professional advisers can identify any potential issues that fall under one of LB&I's active campaigns and work to develop a strategy for addressing that issue throughout the LB&I examination process.

That strategy includes determining who is in the best position to serve as the face of the client in the audit. All communication should flow through that adviser and direct interaction with the client should be limited to the extent possible.

All of this should be done with an eye toward potential future litigation. While future litigation is all about offense, the audit is all about defense, protecting the client by preserving the client's privileges, objections, limitations periods and other statutory protections.

Are You Being Audited by the IRS Wealth Squad?

Read more at: Tax Times blog