Starting in tax year 2020, the new separate Schedule Q (Form 5471), CFC Income by CFC Income Groups, is used to report the CFC's income in each CFC income group to the U.S. shareholders of the CFC so that the U.S. shareholders can use it to properly complete Form 1118 (to compute the high-tax exception, high-tax kickout, and section 960 deemed paid taxes).

On its webpage, the IRS has clarified its instructions for 2020 Schedule Q (CFC Income by CFC Income Groups) of Form 5471 (Information Return of U.S. Persons With Respect to Certain Foreign Corporations).

This update clarifies that:

- Separate Schedule(s) Q (Form 5471) are required to be filed only by Category 4, 5a, and 5b filers. It is not required to be filed by Category 1a or 1b filers. and

- On page 5 of the Instructions for Form 5471, footnote 1 in the table entitled "Filing Requirements for Categories of Filers" does not apply to category 5b filers who are required to complete separate Schedule(s) Q (Form 5471).

IRC Sec. 960(a) provides that, for purposes of computing the foreign tax credit, domestic corporations owning stock in controlled foreign corporations (CFCs) are deemed to have paid a portion of the foreign taxes paid by the CFC.

IRC §904(d)(2)(F)'s “high-tax kickout” rule, for purposes of the separate FTC limitation on passive income, certain high-taxed income that would otherwise be passive income will be treated as general category income.

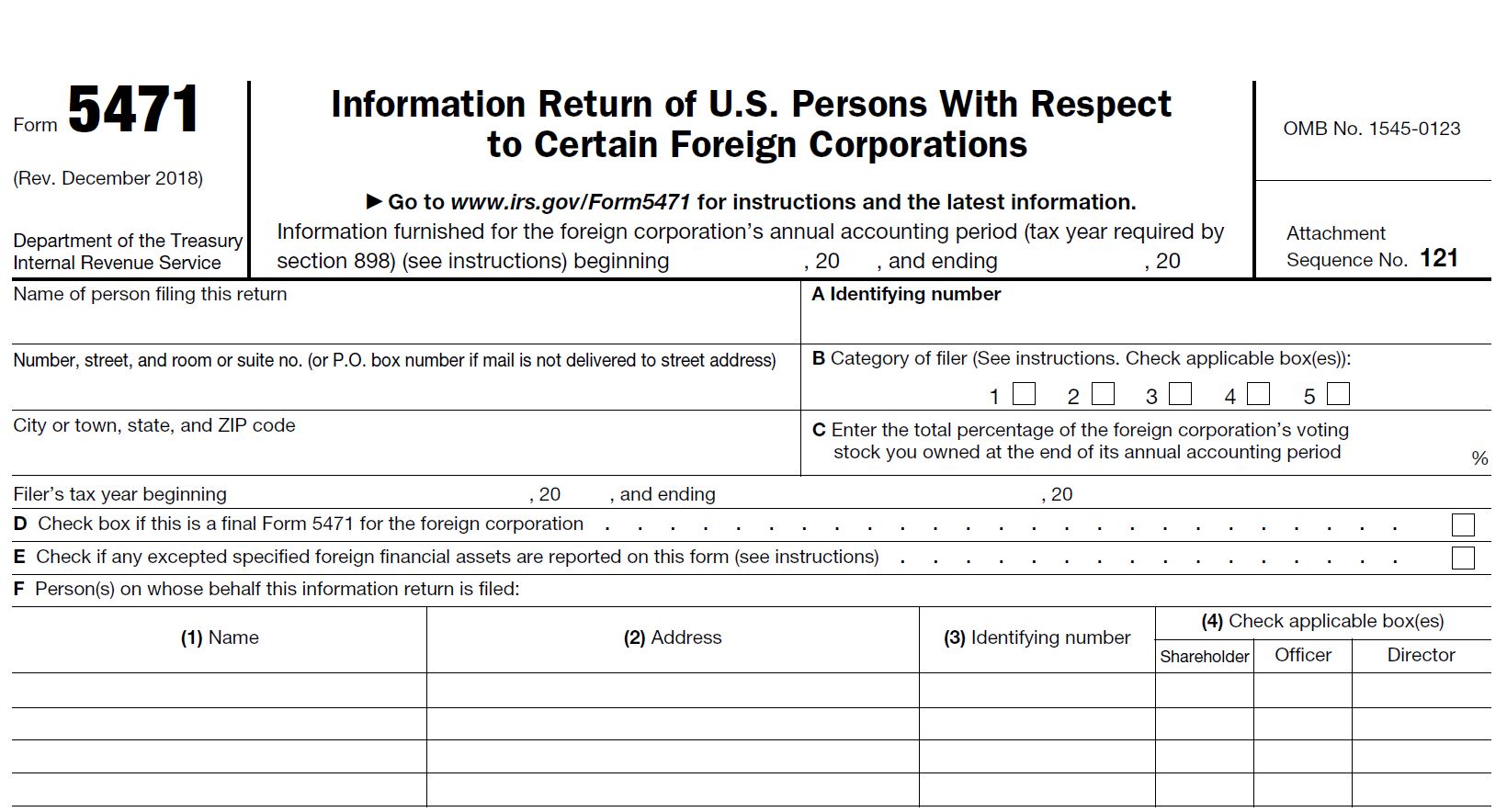

IRC §6038(a)(1) requires U.S. persons to furnish information with respect to any foreign business entity that that person controls on Form 5471, Information Return of U.S. Persons With Respect to Certain Foreign Corporations. Form 5471 lists several categories of persons who must file Form 5471. It also sets out different filing requirements for the different categories of persons.

- Category 1 includes a U.S. shareholder of a foreign corporation that is a IRC §965 specified foreign corporation (SFC) at any time during any tax year of the foreign corporation, and who owned that stock on the last day in that year on which it was an SFC, taking into account the regs under IRC §965. Category 1 is comprised of Categories 1a, 1b and 1c.

- Category 4 includes a U.S. person who had control of a foreign corporation during the annual accounting period of the foreign corporation.

- Category 5 includes a U.S. shareholder who owns stock in a foreign corporation that is a CFC at any time during any tax year of the foreign corporation, and who owned that stock on the last day in that year on which it was a CFC. Category 5 is comprised of Categories 5a, 5b and 5c.

Schedule Q (Form 5471), CFC Income by CFC Income Groups, is used to report the CFC's income in each CFC income group to the U.S. shareholders of the CFC so that the U.S. shareholders can use it to properly complete Form 1118 (Foreign Tax Credit - Corporations) to compute the high-tax exception, high-tax kickout, and Code Sec. 960 deemed paid taxes.

From my discussion with various colleagues, unfortunately tax software four 2020 does not currently provide for the required grouping of income and associated expenses and tax return preparers need to prepare their own spreadsheets to gather this information.

Need Help Filing Form 5471

Contact the Tax Lawyers at

www.TaxAid.com or www.OVDPLaw.com

or Toll Free at 888 8TAXAID (888-882-92

Read more at: Tax Times blog