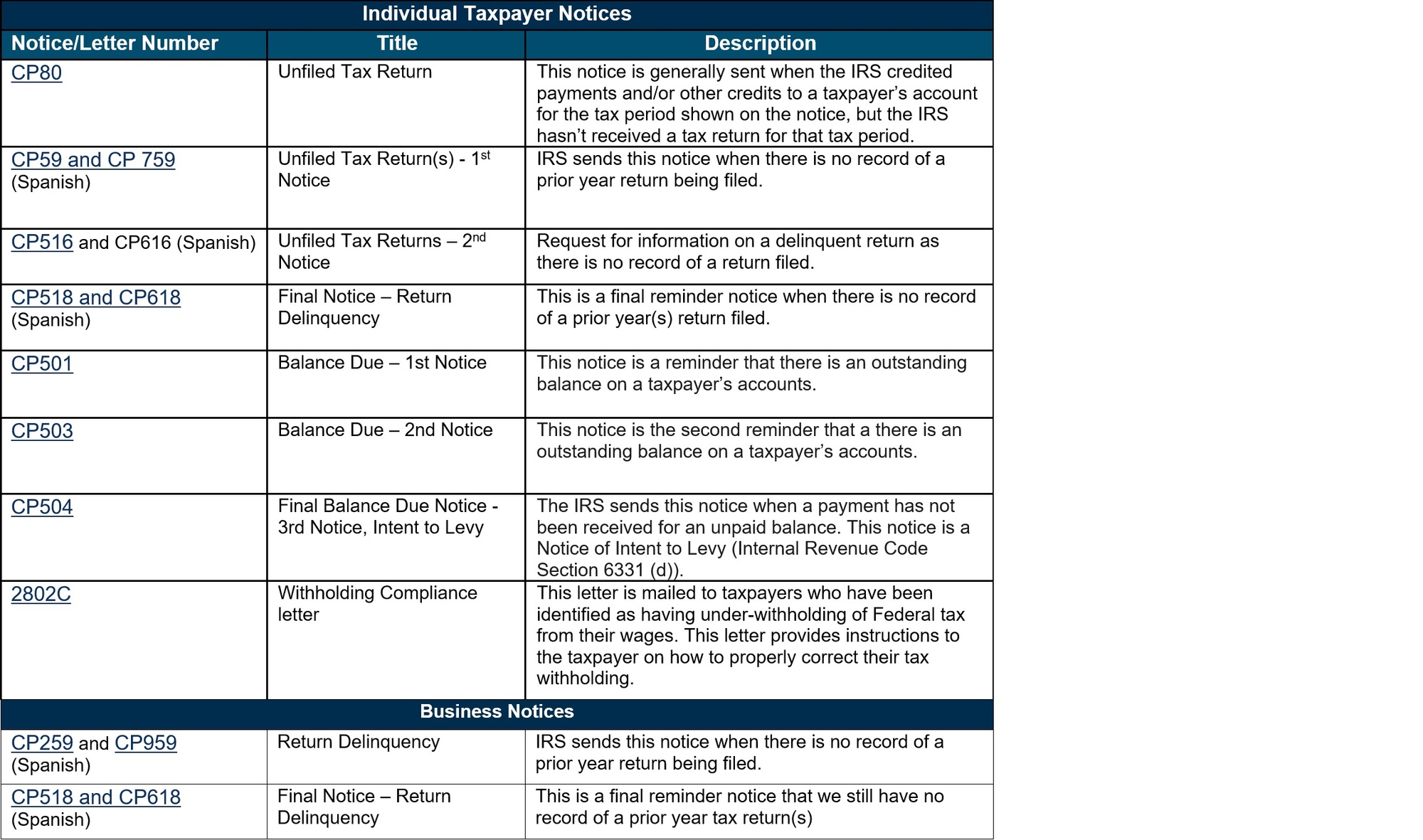

According to IR-2022-31 issued on February 9, 2022, the IRS announced the suspension of more than a dozen additional letters, including the mailing of automated collection notices normally issued when a taxpayer owes additional tax, and the IRS has no record of a taxpayer filing a tax return.

These mailings include balance due notices and unfiled tax return notices. The IRS entered this filing season with several million original and amended returns filed by individuals and businesses that have not been processed due to challenges of the historic pandemic and is taking this step to help avoid confusion for taxpayers and tax professionals.

“Our Efforts Are Not Limited To Suspension of These Additional Letters and the Possibility of Similar Actions Going Forward.

These automatic notices have been temporarily stopped until the backlog is worked through. The IRS will continue to assess the inventory of prior year returns to determine the appropriate time to resume the notices. Some taxpayers and tax professionals may still receive these notices during the next few weeks.

As The IRS Continues To Process Prior Year Tax Returns

As Quickly As Possible.

However, if a taxpayer or tax professional believes a notice is accurate, they should act to rectify the situation for the well-being of the taxpayer. For example, the IRS cautions people with a balance due that interest and penalties can continue to accrue. In addition, IRS employees may in select circumstances issue notices to particular taxpayers to resolve specific compliance issues.

The IRS does not have the authority to stop all notices as many are legally required to be issued within a certain timeframe. The IRS will continue to assess other changes and system modifications that the IRS may be able to implement to assist taxpayers on an array of issues. The IRS will continue to make information available to taxpayers throughout the filing season.

The IRS encourages those who have a filing requirement and have yet to file a prior year tax return or to pay any tax due to promptly do so as interest and penalties will continue to accrue. Visit IRS.gov for payment options.

The suspended notices include:

According to Procedurally Taxing, the IRS is statutorily obligated to send out the notice and demand letter within 60 days after assessment. If it fails to send out the notice and demand letter, the failure does not destroy the assessment but it prevents the federal tax lien from coming into existence. The IRS should continue to send out this letter.

An interesting development is that it is not sending out the statutorily required notice of intent to levy letter required by IRC 6331(d). It doesn’t need to send out this letter unless it intends to levy but without sending out this letter, the last letter in its notice stream, the letter giving Collection Due Process rights, will not allow the IRS to levy. So, even though the IRS does not list the CDP letter (Letter 11) in the list above, it will suspend sending out that letter as well, at least with respect to levies, since sending out that letter will not allow the IRS to levy in the absence of the 6331(d) letter it states here it is going to suspend.

Note that it may have already sent out the 6331(d) letter to someone which would allow it to go ahead with the CDP letter and it states in the notice that it may still be sending out some letters already scheduled.

Have an IRS Tax Problem?

www.TaxAid.com or www.OVDPLaw.com

or Toll Free at 888 8TAXAID (888-882-9243)

Read more at: Tax Times blog