A district court has held in U.S. v. Hughes, (DC CA 10/13/2021) 128 AFTR 2d ¶2021-5309, that a taxpayer's failure to file an FBAR was not willful when she failed to fill out Form 1040's Schedule B, Interest and Ordinary Dividends, which asks about foreign bank accounts. For another tax year, when she did fill out Schedule B, the court found that her failure to file an FBAR was willful.

The penalty for a failing to file an FBAR depending on whether the violation was willful or non-willful. The penalty for a non-willful violation cannot exceed $10,000. (31 USC 5321(a)(5)(B)(i)). The penalty for a "willful" violation cannot exceed the greater of $100,000 or half of the balance of the account at the time of the violation. (31 USC 5321(a)(5)(C)(i))

Ms. Hughes was a bookkeeper and prepared tax returns for herself and for some family members. It was undisputed that Ms. Hughes was required to file FBARs for tax years 2010-2013.

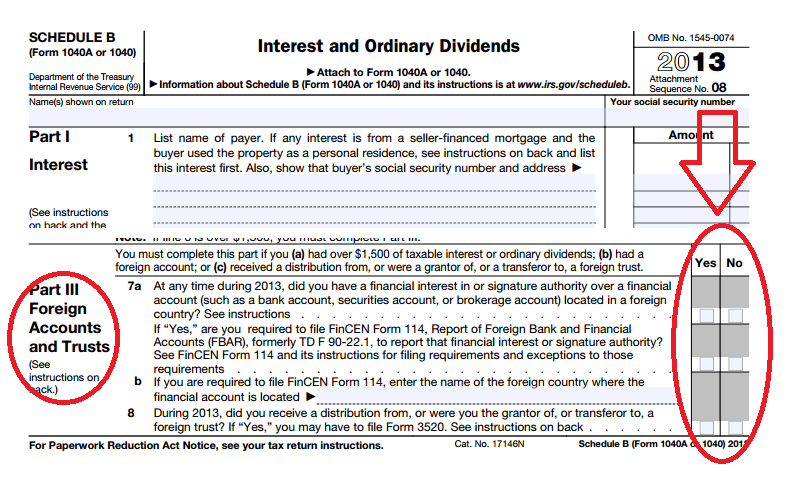

On her 2010 and 2011 tax return which she prepared herself, she failed to fill out Schedule B and she failed to report any of the interest income. Schedule B asks, effectively, if the taxpayer has a foreign bank account and whether the taxpayer needs to file an FBAR.

For 2012 and 2013, she did fill out Schedule B, and answered "yes" to those questions and Included the foreign bank income. But she did not file FBARs. The IRS sought penalties for willful violations for all four tax years.

The District Court Found That Her Failure To File FBARs

In 2012 And 2103 Was Willful.

But Her Failure In 2010 And 2011 Was Not.

The court wrote, "with respect to her 2012 and 2013 returns, there is no doubt that Hughes saw the questions about filing an FBAR, because she answered them... In 2010 and 2011, Hughes's returns did not include Schedule B, so the certification that she 'examined this return and accompanying schedules and statements' does not encompass that schedule and its admonitions about the FBAR. The IRS has identified nothing in Hughes's 2010 or 2011 returns as actually filed that, if 'examined' as she certified, would have put her on notice of the FBAR requirement.

- How about the fact that she intentionally excluded the income from her Form 1040 and she swore that the rest of the return was correct?

- How more intentional can you get than to have a tax return preparer, who knows that the schedule B is required based on the amount of dividend or interest income earned that year, who intentionally leaves out the schedule B?

The court continued, "The circumstances of Hughes's 2010 and 2011 tax returns differ from 2012 and 2013.

Unlike those later years, there is no indication that Hughes reviewed Schedule B, with its instructions regarding the FBAR requirement, in preparing her 2010 and 2011 returns or any time before she did so.

- Very narrow reading of the facts, which completely ignores that she was the tax return preparer who knew a Schedule B, as well as FBAR was required to be filed.

In the absence of any evidence that Hughes was aware of the FBAR filing requirement when she completed her returns for those years, or that she was presented with any information that should have put her on notice of that requirement, the IRS has not met its burden to show that her failure to file FBARs in those years was anything more than negligent."

Have an IRS Tax Problem?

Contact the Tax Lawyers at

www.TaxAid.com or www.OVDPLaw.com

or Toll Free at 888 8TAXAID (888-882-9243)

Read more at: Tax Times blog