- Did your CFC have a lot post 1986 Retained Earnings at the end 2017, which caused it to have a transition tax under IRC section 965?

- Is your CFCs business not doing so well since 2017, as a result of Covid and other economic factors?

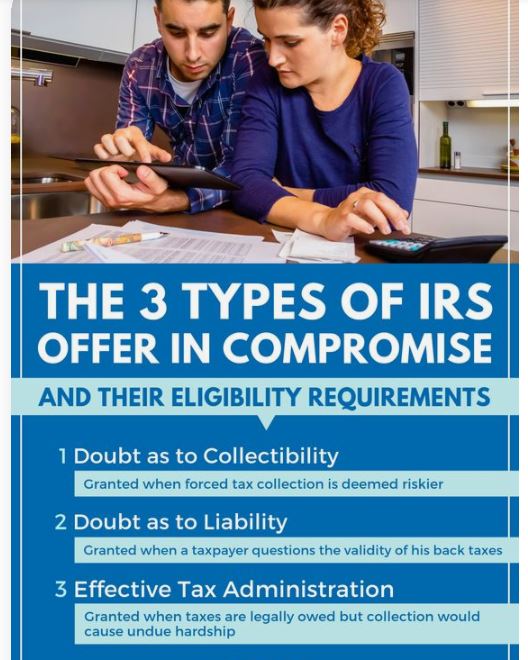

The IRS recentlyreleased guidance on includingtransition tax liabilities under IRC Section965 for settlement under its offerin compromise program. Section 7122 of the Internal Revenue Code authorizes the settlement of Title 26 liabilities, penalties, and interest. Since the transition tax on untaxedforeign earnings is a Title 26 tax, it can be included in a settlement offer.

Under The New Guidelines of IRM 5.8.4.23.7 (09-24-2020)

“IRC §965 (Transition Tax) Liabilities,” if the §965 Liability

Has Been Assessed and No Election Was Made

Under IRC §965(H), the Tax May Be Included in the Offer.

Under the right factual circumstances, an Offer In Compromise may provide an opportunity for settling transition taxes under Section 965.

Since an Offer In Compromise based on Doubt As To Collectability will only be accepted where a taxpayer does not have the ability to pay the tax, you must examine the taxpayer’s financial situation, not just their CFC's financial situation, and consider a taxpayer’s assets, the equity and liability of those assets, the gross income and expenses of that taxpayer. This inquiry includes the valuation of any businesses, business assets, including any foreign businesses or foreign assets of the taxpayer.

As with any Offer in Compromise, the taxpayer must be compliant with their all of their tax filings including FBARs, FACTA requirements, payroll, return filing requirements, and any estimated payments that may be due.

Furthermore, since the Offer in Compromise program only settles Title 26 tax, penalties, and interest, you must consider the timing of the offer in compromise settlement proposal and whether the taxpayer is liable for any FBAR penalties or restitution, as neither FBAR penalties nor restitution can be settled as part of an offer in compromise.

For tax years involving civil tax liabilities and criminal restitution, offers can include the civil tax liabilities, but not the restitution-based assessment. If there are restitution assessments, FBAR penalties, or other non-title 26 liabilities, it is usually in the taxpayer’s best interest to pay off or otherwise resolve those liabilities through installment payment arrangements before submitting an offer in compromise to settle Title 26 liabilities since the payment of the other liabilities will decrease the taxpayer’s available equity in assets and potentially increase a taxpayer’s allowable expenses such that a lower settlement amount may be obtained for the taxpayer through the offer in compromise program.

Have IRS Tax Problems?

Contact the Tax Lawyers at

Marini & Associates, P.A.

Sources

Fla Bar Tax Section Bulletin - Fall 2020

Read more at: Tax Times blog