In United States v. Schwarzbaum (S.D. Fla. No. 18-cv-81147) a federal district court rejected an individual's claims that FBAR penalties assessed against him should be set aside because they were assessed after the limitations period expired.

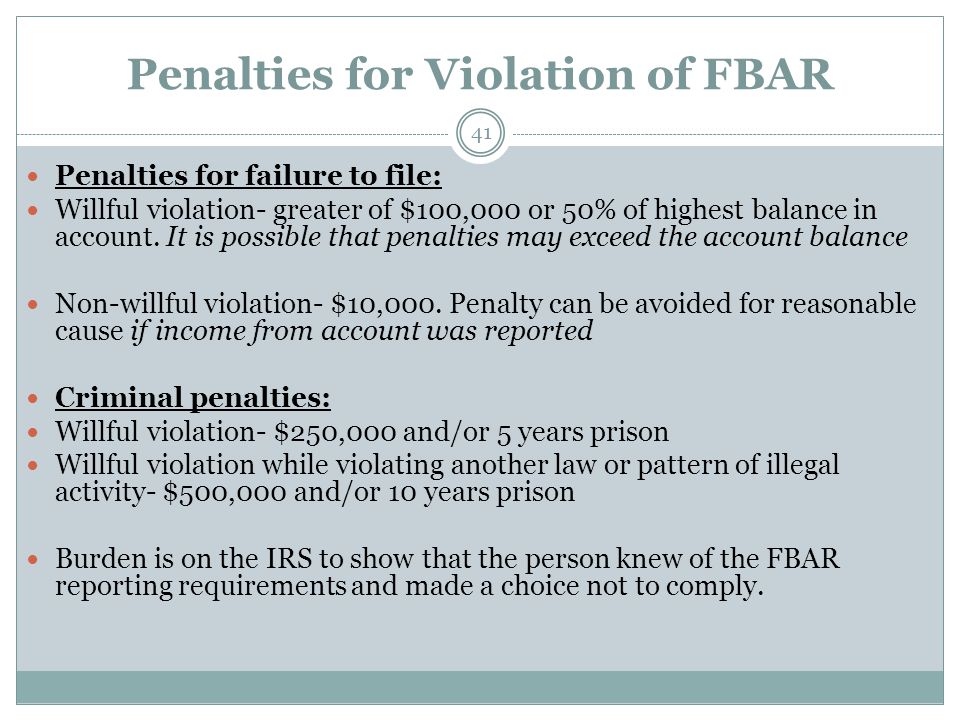

Generally, U.S. persons who maintain a financial account in a foreign country (foreign financial account) must file a Report of Foreign Bank and Financial Accounts (FBAR) with the Treasury’s Financial Crimes Enforcement (FinCEN) division. (31 CFR §1010.350(a)) Willful failure to file an FBAR may result in a penalty. (31 USC § 3521(a)(5)(A)). An FBAR penalty may be assessed at any time before the end of the 6-year period beginning on the date of the transaction with respect to which the penalty was assessed. (31 USC § 5321(b)(1)).

Between 2006 and 2009, the taxpayer, Isac Schwarzbaum, maintained several foreign financial accounts, including accounts in Costa Rica and Switzerland. Isac did not file FBARs for his accounts in Switzerland before 2011.

In 2011, Isac joined the IRS’s Offshore Voluntary Disclosure Initiative (OVDI). As part of his participation in the OVDI, Isac signed an extension of the limitations period to assess and collect taxes and penalties related to his 2006-2009 returns.

Isac then opted out of OVDI and underwent full examinations of his returns. After the examinations, the IRS decided to assert willful FBAR penalties against Isac. Those FBAR penalties (for tax years 2006-2009) were assessed in Sept. 2016.

Isac argued that the FBAR penalty assessments were time-barred. The IRS argued that Isac voluntarily signed a consent to extend the limitations period to assess and collect taxes related to his 2006-2009 returns.

The district court held that Isac’s argument that the FBAR penalties assessed against him were time barred was meritless. The district court found that it was Isac's burden to show that his voluntary agreement to extend the limitations period to assess FBAR penalties was invalid since that was Isac’s affirmative defense. However, Isac failed to point to any legal authority to support his argument that the agreement he signed was invalid. (See Pages 8-9):

- To the extent that Schwarzbaum argues that the penalties are time-barred, the argument lacks merit. Although Title 31 does not expressly authorize the extension of the applicable statute of limitations by agreement, it does not expressly prohibit such extensions. Schwarzbaum has failed to point to any legal authority indicating that such extensions would be improper. See Melford v. Kahane & Assocs., 371 F. Supp. 3d 1116, 1126 n.4 (S.D. Fla. 2019) (“Generally, a litigant who fails to press a point by supporting it with pertinent authority, or by showing why it is sound despite a lack of supporting authority or in the face of contrary authority, forfeits the point. The court will not do his research for him.”) (internal quotations and citation omitted).

- Notably, Schwarzbaum does not dispute that he signed consents agreeing to extend the time during which FBAR penalties could be assessed and collected. See ECF Nos. [44-5], [44-6], [44-7].

- Rather, in his Reply he acknowledges the lack of authority, argues that the USA relies upon three irrelevant cases in its Response, and then endeavors to distinguish them.

- However, Schwarzbaum ignores that it is he who bears the burden of establishing the defense of statute of limitations in the first instance. See, e.g. Feldman v. Comm’r of Internal Revenue, 20 F.3d 1128, 1132 (11th Cir. 1994) (“When a taxpayer raises the affirmative defense of the statute of limitations, the taxpayer bears the burden to prove that defense.”) (citation omitted).

- Here, Schwarzbaum has failed to provide any authority to support his argument that an agreement to extend the time to assess FBAR penalties under Title 31 is invalid.

Have Undeclared Income from an Offshore Bank Account?

Want to Know Which OVDP Program is Right for You?

Contact the Tax Lawyers at

Marini& Associates, P.A.

for a FREE Tax Consultation

at: www.TaxAid.com or www.OVDPLaw.com or

Toll Free at 888-8TaxAid (888) 882-9243

Read more at: Tax Times blog

{kind=link}