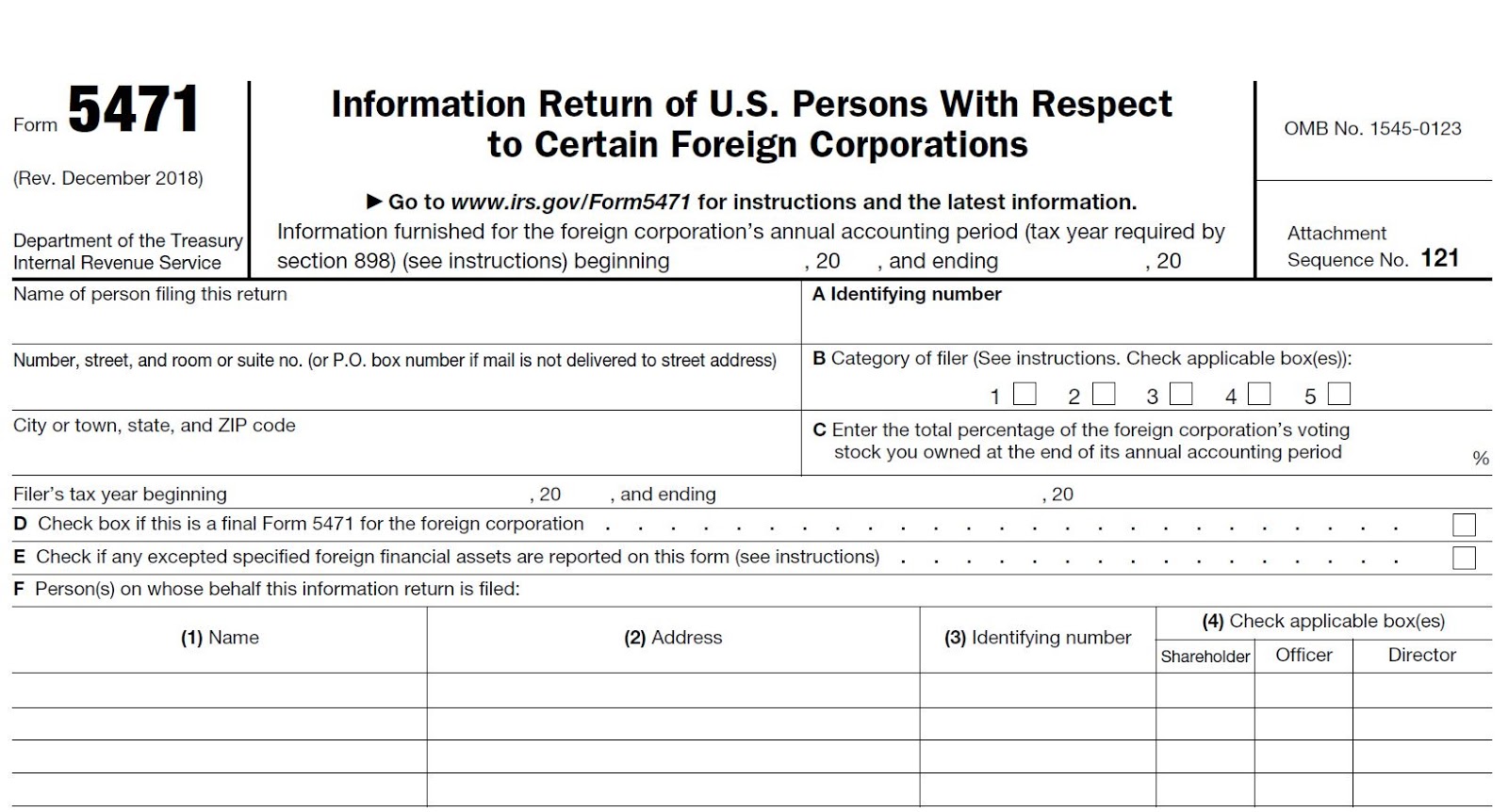

On October 2, 2019, we posted IRS Grants Relief for Certain Foreign Stock Ownership! where we discussed that new regulations from the Internal Revenue Service provide relief to some U.S. taxpayers who own stock in certain foreign corporations. Rev. Proc. 2019-40 and the proposed regulations limit the inquiries required by U.S. taxpayers to determine whether certain foreign businesses are controlled foreign corporations.

On October 2, 2019, we posted IRS Grants Relief for Certain Foreign Stock Ownership! where we discussed that new regulations from the Internal Revenue Service provide relief to some U.S. taxpayers who own stock in certain foreign corporations. Rev. Proc. 2019-40 and the proposed regulations limit the inquiries required by U.S. taxpayers to determine whether certain foreign businesses are controlled foreign corporations.

Now according to Law360, The Internal Revenue Service proposed regulations on October 1, 2019 to provide some relief and restore continuity after a change under the 2017 federal tax overhaul that broadened the scope of offshore subsidiaries treated as controlled foreign corporations.

The proposed regulations are generally intended to ensure that the operation of certain rules is consistent with their application before the Tax Cuts and Jobs Act repealed Internal Revenue Code Section 958(b)(4) . Before it was removed, the measure had prevented the so-called downward attribution of stock ownership of overseas corporations from foreign parent companies to U.S. affiliates.

Under Section 958(b)(4), a foreign parent company's ownership of an offshore subsidiary wasn't attributed to the parent company's U.S. affiliate. With Section 958(b)(4) gone, however, the offshore subsidiary is treated as a controlled foreign corporation, or CFC, under the U.S. branch.

In the absence of the proposed rules, these corporate groups' foreign subsidiaries could potentially have been designated as CFCs, which would result in all or part of the foreign subsidiaries' earnings, depending on the industry, being treated as U.S. source income.

“Comments received suggested that such treatment would render companies’ business models untenable,” the IRS said.

Is A CFC Is Made Without Regard

Read more at: Tax Times blog