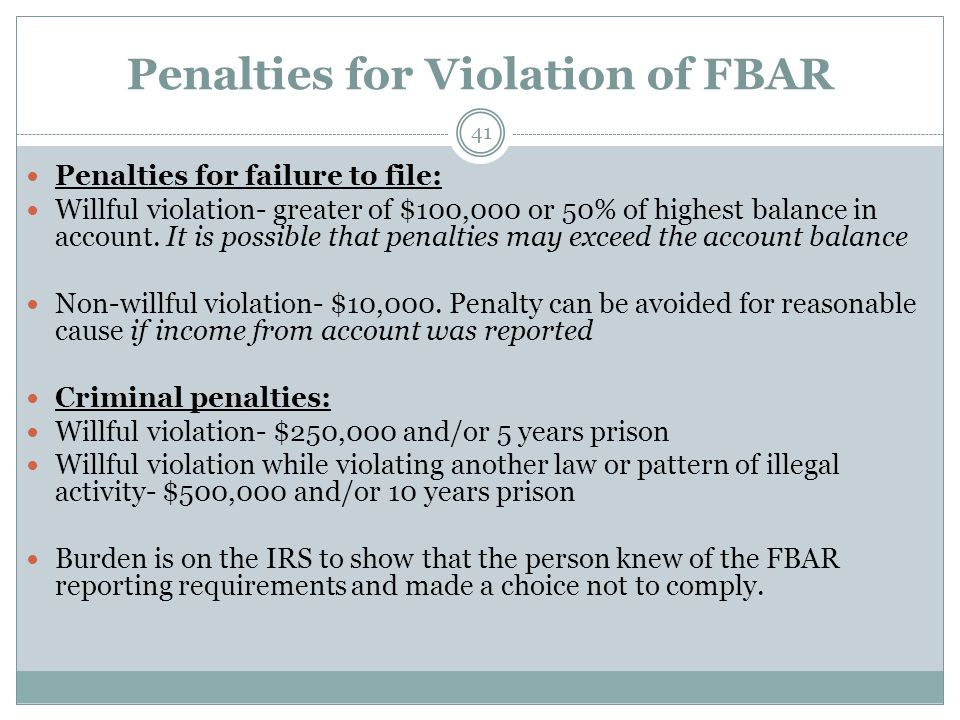

On March 30, 2021 we posted Appeals Court Rules That Non-Willful FBAR Penalty Applies Per Form, Not Per Account, where we discuss that the Court of Appeals for the Ninth Circuit, reversed the district court decision and has held that the $10,000 non-willful FBAR penalty (for failure to file the FBAR) applies per FBAR form, not per the number of financial accounts (e.g., bank accounts) required to be reported on the form in

Now according to Law360, in U.S. v. Alexandru Bittner, ,case number 20-40597, in the U.S. Court of Appeals for the Fifth Circuit, the court ruled on that the $10,000 maximum penalty for a nonwillful failure to file a foreign bank account report applies to each account, not each year, reversing a lower court's decision and diverging from the Ninth Circuit.

The lower court's decision that the penalty applied for each failure to file an annual FBAR was inconsistent with the Bank Secrecy Act and corresponding regulations, the three-judge panel said.

To Report Each Foreign Account,"

U.S. Circuit Judge Stuart Kyle Duncan Said In The Court's Unanimous Opinion.

The opinion noted the panel's disagreement with a Ninth Circuit decision in March that found a California woman was liable for only one Internal Revenue Service-assessed penalty for each annual, nonwillful failure to file an FBAR. Earlier in November, the federal government accepted her undisclosed settlement offer.

The IRS Had Levied The Penalties For Each Of Bittner's Unreported Accounts Every Year From 2007 To 2011.

The IRS assessed the penalties in 2017 and sued him in 2019 over the late forms, according to court documents. A Texas federal judge in June 2020 lowered the assessed penalties to $50,000, saying the $10,000 cap on penalties applied to each year.

The Fifth Circuit, however, disagreed with the district court's view that a violation of Section 5314 of Title 31 is directly tied to the obligation the statute imposes, which is the filing of a single report per year. Further, the lower court's view would lead to a result unattached from the statute, the appeals court said.

Bittner was born in Romania, immigrated to the U.S. and became a naturalized citizen, and then returned to Romania, where he became a successful businessperson and investor, according to the Fifth Circuit opinion. While there, he earned millions of dollars and bought interests in companies, including in real estate, construction and manufacturing, the opinion said.

Bittner's business abilities were a factor in the Fifth Circuit's rejection of his claim that the lower court was wrong to deny his defense that he had reasonable cause for failing to report his foreign accounts.

"Bittner's business savvy makes his failure to inquire about his reporting obligations even more unreasonable," Judge Duncan said.

Judge Duncan also said Bittner failed to demonstrate he had exercised ordinary business care and prudence regarding reporting requirements, noting he admitted to doing nothing to comply with them.

The Fifth Circuit affirmed the lower court's decision that Bittner was liable for failing to report accounts, and its rejection of his reasonable cause defense. The panel vacated and remanded the case for further proceedings.

Read more at: Tax Times blog

{kind=link}